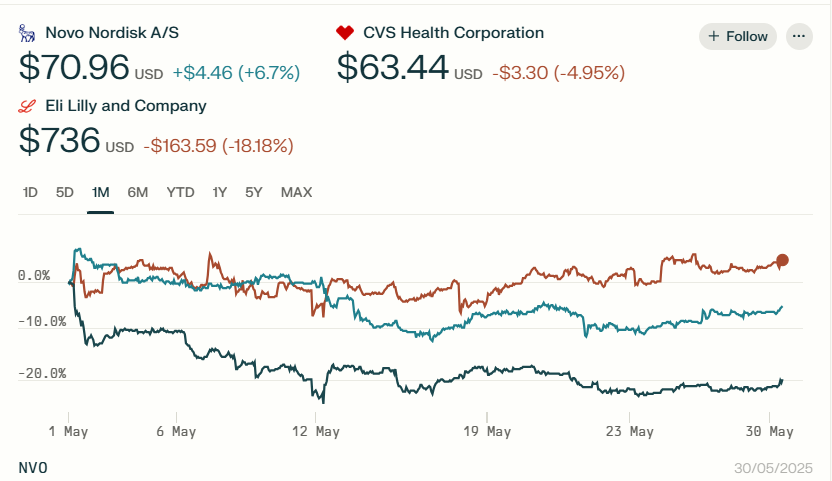

Eli Lilly & Co. (LLY) shares have come under significant pressure in late May following a pivotal decision by CVS Health’s Caremark, one of the largest pharmacy benefit managers (PBMs) in the United States.

Effective July 1, 2025, CVS Caremark will designate Novo Nordisk’s (NVO) Wegovy as its preferred GLP-1 weight-loss drug on its largest commercial template formularies, a move that will exclude Eli Lilly’s popular obesity treatment, Zepbound.

This strategic shift by CVS Caremark, which manages prescription drug coverage for millions of Americans, has sparked investor concern over Zepbound’s future sales growth and market share. Zepbound, a cornerstone of Eli Lilly’s rapidly expanding portfolio, generated $2.3 billion in sales in the first quarter of 2025 alone.

The exclusion from CVS’s standard formulary could make it more challenging for some patients to access Zepbound, as insurance coverage heavily influences medication affordability and choice.

Following the announcement, Eli Lilly’s stock experienced a notable decline, reflecting fears of a potential slowdown in Zepbound’s impressive market penetration, where it had recently overtaken Wegovy in weekly U.S. prescriptions.

While Eli Lilly reported strong overall first-quarter revenue of $12.73 billion, a 45% increase year-over-year driven by Mounjaro and Zepbound, the CVS news overshadowed these positive results. The company had previously revised its full-year adjusted profit forecast downward, citing deal-related charges, though its sales forecast remained robust.

Analysts note that while Zepbound has demonstrated strong efficacy, the PBM landscape and negotiated pricing play a critical role in the highly competitive weight-loss drug market.

Eli Lilly has stated it is not pursuing exclusive “one-of-one” agreements with PBMs and aims to set list prices closer to what it expects health plans will ultimately pay. The company continues to invest heavily in U.S. manufacturing capacity, committing $27 billion to boost production of its key drugs.

However, the CVS Caremark decision introduces a new dynamic, potentially intensifying the competition with Novo Nordisk and requiring Lilly to navigate evolving formulary landscapes to maintain Zepbound’s growth trajectory. The market will be closely watching how this development impacts Lilly’s market share, which stood at over 50% in the U.S. GLP-1 drug market prior to this change.