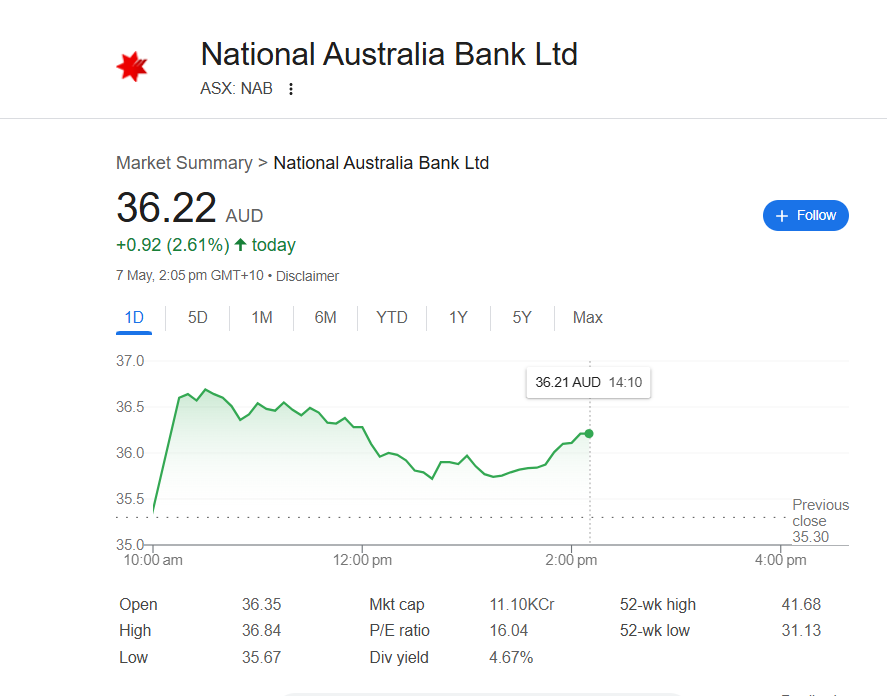

National Australia Bank (NAB) shares climbed over 3% in early trading on Wednesday after the bank reported a first-half profit that surpassed market expectations, underscoring its resilience amid a fiercely competitive lending environment and persistent global economic uncertainty.

NAB, Australia’s largest business lender, posted cash earnings of $3.58 billion for the six months ended March 31, 2025, reflecting a 1% increase from the same period last year. The result outpaced analyst forecasts and was well received by investors, with the NAB share price rallying to $36.42, up 6.3% over the past 12 months.

The bank declared an interim dividend of 85 cents per share, up from 84 cents a year ago, returning $2.6 billion to shareholders-many of whom are retail investors relying on dividend income. Statutory net profit came in at $3.41 billion, a 2.5% decline year-on-year, reflecting the bank’s preference for cash earnings as a more accurate measure of underlying performance.

NAB’s net interest margin (NIM), a key profitability metric, remained steady at 1.70%. However, when excluding a modest boost from markets and treasury operations, the underlying margin contracted by 3 basis points. This pressure was attributed to heightened competition for deposits and mortgages, as well as increased wholesale funding costs.

Despite the margin squeeze, NAB’s operational performance was bolstered by disciplined cost management and robust growth in both business lending and customer deposits. Gross loans and advances rose by 2.5%, while deposits grew by 4.1%, outpacing lending growth and further strengthening the bank’s balance sheet.

Expenses increased by 1.4%, primarily due to higher personnel costs, financial crime compliance, and ongoing investment in technology. These were partially offset by productivity gains and lower costs related to regulatory compliance.

Business and Private Banking remained the largest contributor to profits, with earnings in this segment rising 1.4% to $1.63 billion. Corporate and Institutional Banking also saw a 4.1% increase in earnings, while New Zealand Banking posted a 12.5% gain in local currency terms. Personal Banking, however, recorded a 6.8% decline in earnings, reflecting continued margin compression in the mortgage market.

NAB CEO Andrew Irvine, in his first half-year report since taking the helm, acknowledged the “challenging operating conditions” and pointed to escalating global trade tensions as a significant source of uncertainty for the economic outlook. Irvine emphasized that the bank’s conservative balance sheet and strong risk settings would help it navigate potential headwinds, including the prospect of further international trade disruptions.

Looking ahead, NAB remains optimistic about the underlying growth prospects for the Australian and New Zealand economies, supported by easing inflation, potential interest rate cuts, and resilient household consumption. The bank expects these factors to underpin continued lending growth, particularly to small and medium-sized businesses, even as business owners remain cautious about taking on new debt.

With a clear strategy focused on growing its core business banking franchise, driving deposit performance, and improving proprietary home lending, NAB appears well positioned to sustain its competitive edge and deliver value to shareholders in the months ahead.