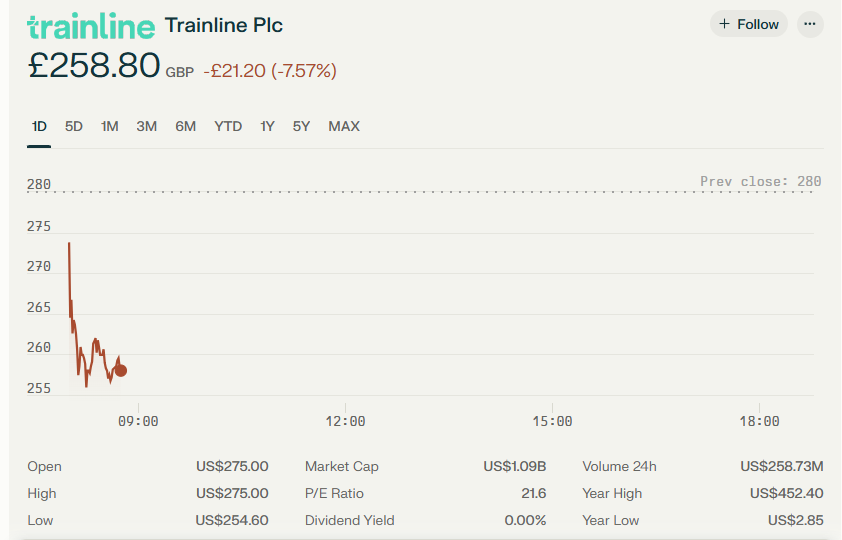

Trainline shares tumbled just over 7% to 260p on Wednesday, deepening a year-to-date decline that now approaches 20%. The drop came despite the rail ticketing platform reporting robust growth in its latest financial results, as investor sentiment remains clouded by concerns over the outlook for UK and European tourism.

For the year ended 28 February 2025, Trainline posted a 12% rise in net ticket sales to £5.91 billion and an 11% increase in group revenue to £442 million. Adjusted EBITDA surged 30% to £159 million, while operating profit climbed 54% to £86 million.

UK consumer sales grew 13%, and international B2B API sales jumped 63%, highlighting the company’s expanding footprint both domestically and abroad.

Despite these strong operational metrics, the share price reaction was muted. Much of the positive performance had already been flagged to the market in March, and investors appear to be focusing on external risks.

Pessimism about the near-term prospects for travel and tourism, particularly in the UK and across Europe, continues to weigh on sentiment. Concerns include potential slowdowns in consumer demand, ongoing economic uncertainty, and the possibility of softer growth in key international markets.

Shore Capital, which maintains a ‘Buy’ rating on Trainline, noted that the current share price reflects a significant amount of “bad news” already being priced in. The broker highlighted that Trainline remains well-positioned to scale its business both at home and internationally, pointing to its recent success in Spain, where net ticket sales have nearly tripled over two years and market share on top routes has more than doubled.

Looking ahead, Trainline projects net ticket sales growth of 6% to 9% for the next financial year, though it anticipates revenue growth will lag behind, at 0% to 3%, due to a higher mix of lower-margin, short-distance travel. Adjusted EBITDA is expected to rise by 6% to 9%, reflecting continued cost discipline and operational leverage.

While Trainline’s fundamentals remain solid, the share price performance underscores the market’s caution in the face of macroeconomic headwinds and sector-specific uncertainties. The company’s ability to deliver on its growth ambitions, particularly in Europe, will be closely watched by investors seeking signs of renewed confidence in the months ahead.